December 2024 FOMC Meeting Postmortem

The Fed cut rates today, but post-meeting statement, updated forecasts and press conference suggest a lot less easing, if at all, is in the pipeline for 2025.

As expected, the Fed cut rates by 25bps but it used the post-meeting statement, forecast updates and press conference to signal its concern with slowing disinflation momentum and heightened policy uncertainty. We likely will have a pause at the January FOMC meeting followed by a more wide-ranging re-assessment of the Fed’s outlook after the March FOMC meeting once there’s more clarity with regards to new economic policy measures from the new administration in DC. A substantial slower pace of policy rate easing beyond today is pretty much certain now; we might see the end of easing cycle at some point in H1 2025.

Key takeaways:

The FOMC cut the Fed funds target range by 25bps to 4.25%-4.50%. There was no change in the pace of reductions of the Fed’s holdings of Treasury and mortgage-backed securities. There was, as in September, one dissenter; this time Fed President Hammack preferred to stay on hold rather than to cut again, with three non-voting FOMC members also preferring to stay on hold.

The statement following made future rate decisions even more data dependent than usual. While there might be lower rates in the near future, the Fed is quickly approaching the point at which it is ready to end the easing cycle.

Many FOMC members shifted back towards a greater concern regarding inflation than with regards to the labor market.

Rate cuts at the March and June FOMC meetings are now the modal expectation. While favorable based effects for year/year PCE inflation will support the March rate cut, by the May meeting the Fed will have more inflation data in hand to assess if more disinflation beyond base effects is driving the data or not. If not, there will be no more rate cuts beyond March for a while.

Decision, Post-Meeting Statement and Post-Meeting Press Conference

As expected, the FOMC decided to lower for the third consecutive month the Fed funds rate target range to 4.25%-4.50%. The post-meeting statement made future rate decisions even more data dependent than usual:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Since earlier in the year, labor market conditions have generally eased, and the unemployment rate has moved up but remains low. Inflation has made progress toward the Committee's 2 percent objective but remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to

4-1/2 to 4-3/44-1/4 to 4-1/2 percent percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly;

Beth M. Hammack; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Voting against the action was Beth M. Hammack, who preferred to maintain the target range for the federal funds rate at 4-1/2 to 4-3/4 percent.FOMC Statement, December 18, 2024 (with annotations relative to the November FOMC statement).

As was the case at the September FOMC meeting there was one dissenter, which at this meeting was newly minted Cleveland Fed President Hammack.

Chair Powell’s remarks confirmed that with this rate cut the recalibration phase has concluded. This is something that I have quantified in my previous pieces on Fed policy, where using a policy rule exercise I showed that at the time of the September FOMC meeting the Fed funds rate was ~100 bps too high. With both core inflation and the unemployment rate moving sideways since that meeting, subsequent cuts at the November and December meetings have given the Fed the opportunity to calibrate its policy rate in line with fundamentals.

Regarding the next phase, Chair Powell was a lot less forthcoming. Although the Chair referred to a number of indicators that suggested continued labor market cooling, he did also sound less worried about a further deterioration of the labor market. In terms of inflation, he did attempt to sound similarly less worried. However, when questioned whether members had conditioned on potential policy action of the incoming new administration, he had admitted quite a few had done that and that this resulted in more adverse inflation outlook for these FOMC members. Given the relatively large dissenting faction at this meeting, one voting member and three non-voting members, it does seem that we are on the verge of another shift in the Fed’s policy preferences: from minimizing the fallout of labor market back to more concern regarding sticky inflation.

The Fed’s Own View

FOMC members updated their forecasts for inflation, growth the unemployment rate and the Fed funds rate at this meeting. The inflation outlook was modified relative to September, where the 2024 Q4/Q4 core PCE inflation projection was upgraded to 2.8% from 2.6% previously (back to where this forecast was at the time of the June FOMC meeting). Beyond 2024 the Q4/Q4 core PCE inflation projections also moved up for 2025 from 2.2% to 2.5% as well as for 2026 from 2% to 2.2%. Achieving the 2% inflation target is becoming increasingly uncertain for the Fed. The Fed needs to be careful with this kind of signaling as it could start to erode its medium-term credibility.

The SEP projections for the unemployment rate moved down substantially relative to the September SEP: from 4.4% to 4.2% in 2024, and from 4.4% to 4.3% in 2025. Basically, the Fed now expects the unemployment rate to stay put at its long-run level throughout the forecast horizon.

The median Fed funds projection for 2025 in this updated SEP increased 50bps relative to September, from 3.4% to 3.9%, implying that the number of rate cuts for 2025 was dialed down from four cuts to two, more than I was expecting. Similarly, the Fed funds projection for 2026 was upgraded by 50bps from 3% to 3.4%. With a new long-run Fed funds rate at 3%, this means that the Fed now expects to be restrictive through 2026.

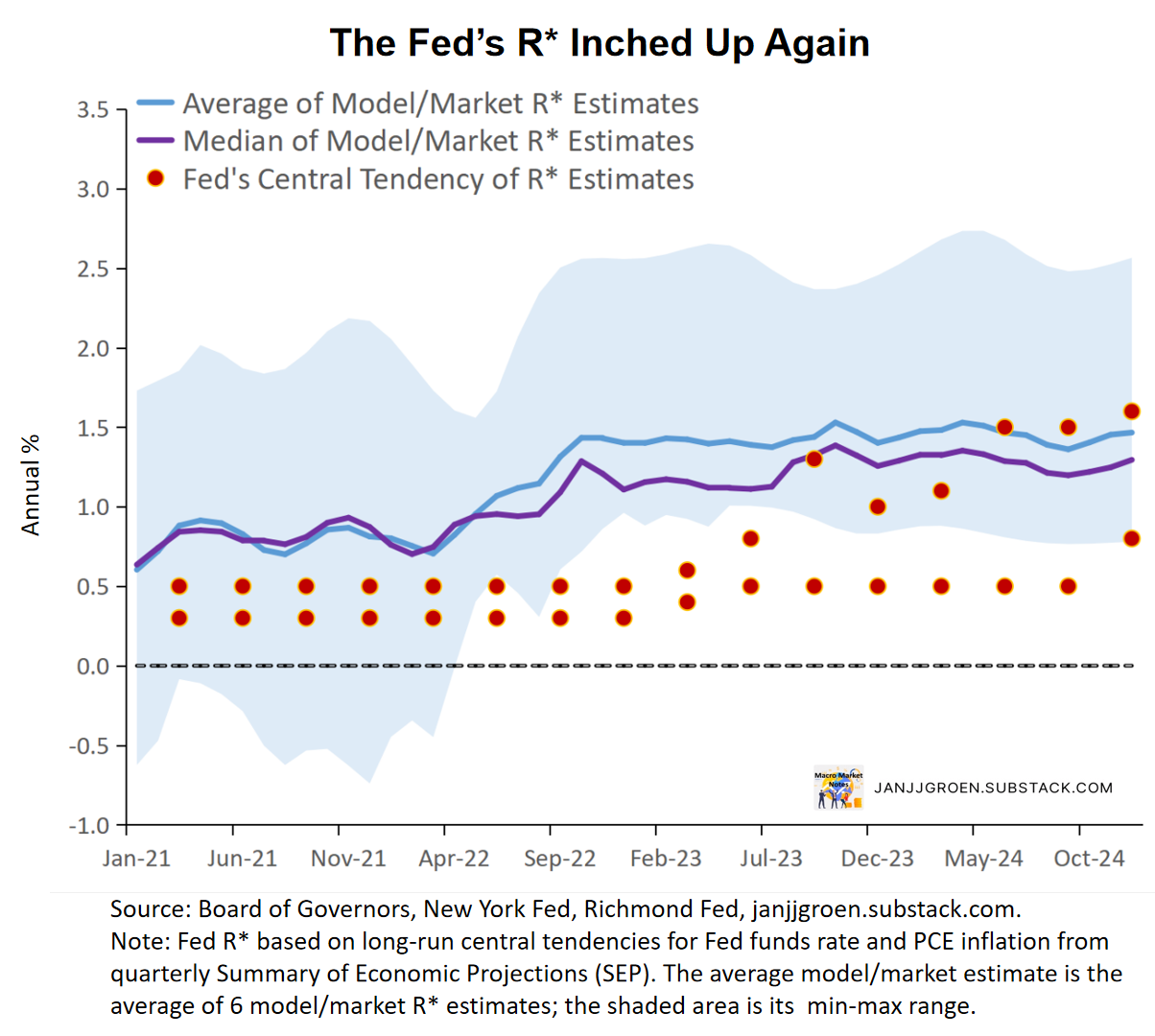

The Fed’s quarterly Summary of Economic Projections (SEP) provides a clue about the range of views within the FOMC on R*, using the central tendency for the longer run Fed funds rate and PCE inflation, respectively. The chart above suggests that compared to September the distribution of FOMC members’ own assessment of the neutral real rate inched up again, with the median changing from 0.9% previously to 1% now. The Fed’s R* uncertainty remains high, with increasingly more FOMC members’ estimates converging towards to those from models and market data.

The chart above contrasts my surveys-based one-year real rate relative to the average of model- and market-implied R* estimates with a proxy of the Fed’s view on this real rate gap using information from its own SEP. This chart suggests that since the September FOMC meeting policy stance expectations from “Main Street” and markets have increased in restrictiveness over the one-year horizon. There clearly is more disagreement amongst FOMC members with regards to the degree of restrictiveness of their policy stance over that horizon.

Beyond Today’s Meeting

In my December FOMC preview I noted that while disinflation momentum seemed to have waned in the data, the uncertain with regards to the new economic policies of the new administration in DC would mean more neutral future policy guidance from the Fed. Consequently, I was expected only a modest dialing back of future rate cuts. That clearly did not happen. In fact, quite a few FOMC members already have started make assumptions about these new policies, which led many FOMC members to significantly tilt risks around their inflation outlook to the upside. In the updated SEP the diffusion index for the core inflation risk weighting rose notably to a level not seen since the September 2023 FOMC meeting (chart above). Similarly, the risk diffusion index declined markedly for the unemployment rate outlook. Inflation will now be the main focus again for the Fed funds rate setting policy, a change from the labor market focus that has dominated since the summer.

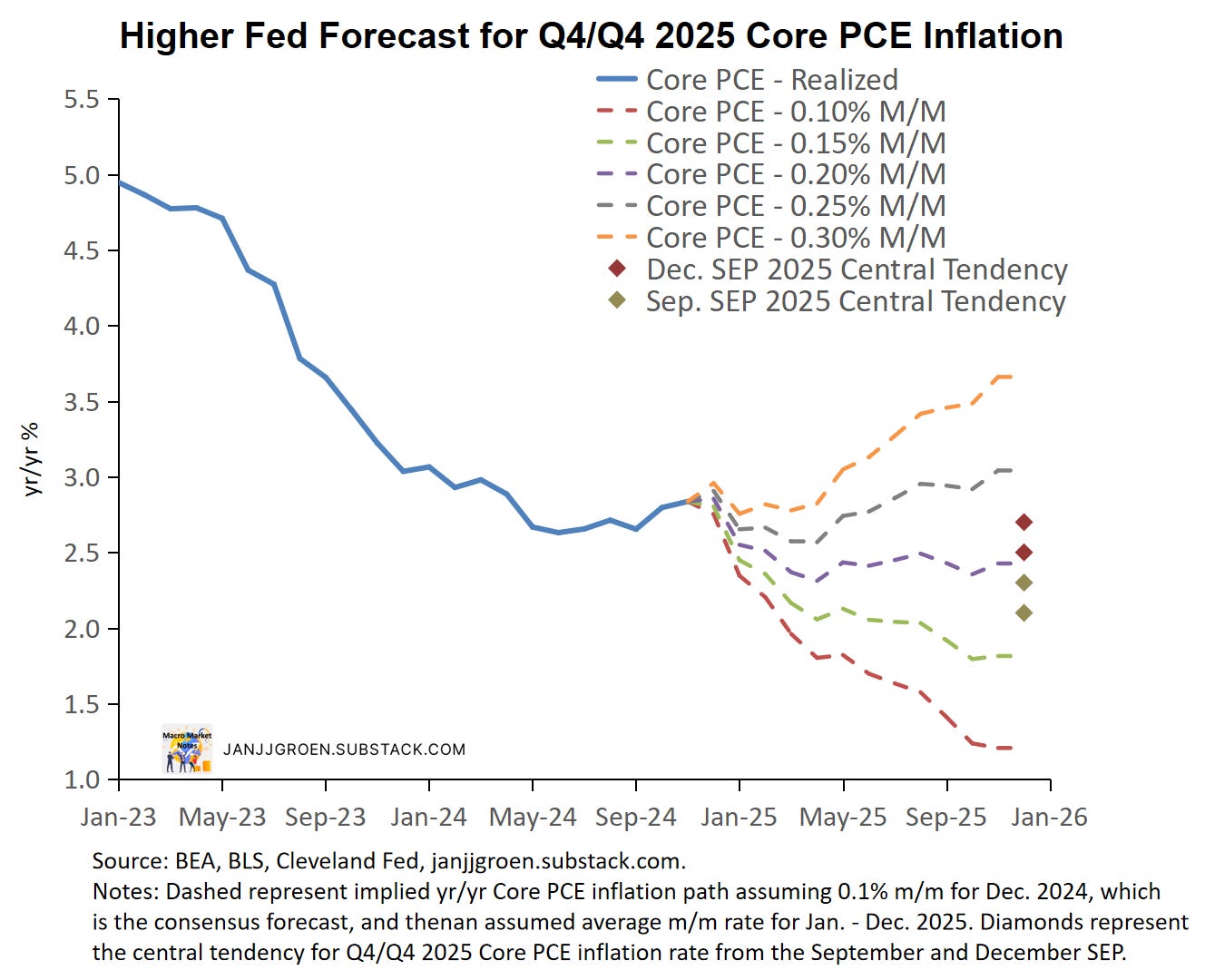

As a consequence, the central tendency of the Q4/Q4 2025 core PCE inflation projection shifted up significantly, as can be seen in the chart above. Where in the September SEP these central tendencies implied an average month/month core PCE inflation rate for 2025 well below 0.2%, the December update moved them well above (chart above) with likely a number of FOMC members probably penciling in a close to 3% Q4/Q4 2025 core PCE inflation rate.

The chart above also provides a clue about the timing of the two rate cuts that are implied by the December SEP. On balance, favorable base effects imply under most assumptions regarding the average monthly inflation a slowdown in the year/year core PCE inflation rate well into H1 2025. The chart above also suggests that the moderate inflation paths, those with an average month/month rate of 0.2% or less for 2025, will start to dip below 2.5% by March.

This to me suggests two things: (i) that as of now we’ll see a rate cut every other meeting between today and June, with 25bps rate cuts in March and June, and (ii) the May meeting becomes a “risk meeting” as by then FOMC members will have enough data to assess whether inflation for the remainder of 2025 will be moderate enough or not, and if not that might mean no more rate cuts beyond March for a while.