May 2025 FOMC Meeting

Given elevated underlying inflation and a resilient labor market the Fed was bound to stay on hold. Today's meeting confirmed it will be on hold for a while.

Today’s May 2025 FOMC meeting decision was as expected, as was the signaling that came out of the post-meeting statement and press conference.

Key takeaways:

The FOMC kept the Fed funds target range unchanged at 4.25%-4.50%. The pace of reductions of the Fed’s holdings of Treasury and mortgage-backed securities also did not change.

The post-meeting statement singled out even more than in the previous statement the uncertainty in the economic environment due to the current administration’s tariffs policy.

Post-meeting remarks by the Chair suggests that with the economy currently still in a fairly good shape, the Fed can be patient and assess how the administration’s policies will adversely impact the Fed’s dual mandate. Incoming data will be monitored from meeting-to-meeting to decide to either cut rates or keep them on hold.

Given that the large-scale tariff hikes will likely more quickly impact inflation than the labor market, and that the already elevated inflation expectations could make this inflation impact more persistent, it’s very unlikely that the Fed will change policy rates this year.

Preamble

At the March FOMC meeting FOMC widely upgraded their inflation projection owing to the likely impact of forthcoming tariff hikes and signaled a prolonged pause in rate cuts to assess how elevated policy uncertainty would unwind over the course of the year. The arrival of '“Liberation Day” indicate a worse than expected (from the perspective of the FOMC) range of tariff hikes and trade policy uncertainty did not unwind but instead remained elevated as the Trump Administration first raised the tariff hikes on China further and then later on announced a 90 day “pause” where most countries saw their new tariffs temporary pegged at 10% except for China. According to the Yale Budget Lab, after “Liberation Day” and the subsequent “pause” the U.S. currently faces an average effective tariff of about 28% on imported goods, with tariffs heavily skewed towards Chinese imports, which over time will likely decline to 18% as consumption patterns adapt and imports shifts across countries. In March, on the eve of “Liberation Day”, the average effective tariff on goods imports was about 2.5%.

In the meantime, data releases gave mixed signals:

Although the preliminary Q1 estimate of GDP suggested that the U.S. economy shrank slightly, this mainly reflected a surge in imports (which adversely impacted GDP through a severely negative net export contribution) as both firms and consumers pulled forward purchases to stay ahead of upcoming tariff hikes. Indeed, real final sales to private domestic purchasers (i.e., the sum of real consumption and real private fixed investment) grew at about the same pace as in Q4: 3% AR vs. 2.9% AR previously, although compared to Q4 consumption slowed over the quarter whereas investment spending picked up.

The slowdown in Q1 consumption was mainly due to negative consumption growth in January, by March the pace of real consumption growth had picked up again on account of strong durable goods consumption (tariff fears-induced pull forward spending!) and rebounding services spending.

In April, jobs growth remained solid although underlying trends suggested that payrolls growth is not high enough to keep the future unemployment rate from moving up as underlying labor demand is slowing.

Household sentiment surveys have been deteriorating since the fall (see here and here), on account of higher inflation expectations, more downbeat future income expectations and a gloomier labor market outlook. This household confidence decline lined up with a slowing in household labor income growth from the ‘hard data’.

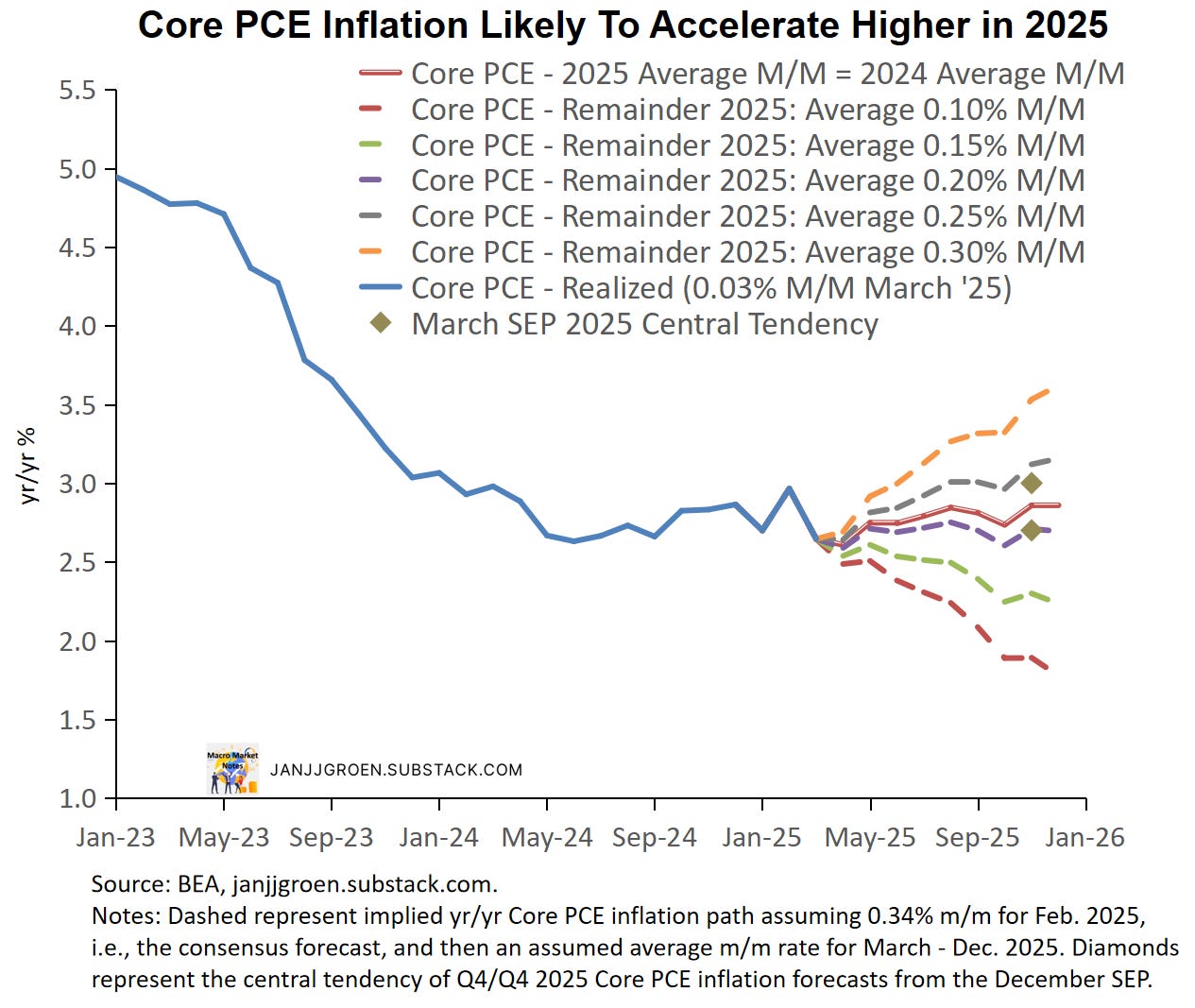

While core PCE inflation slowed in March, underlying PCE inflation trends also eased but remain well above the Fed’s 2% inflation target.

The most worrying signal from the consumer sentiment data for the Fed was that inflation expectations in both the University of Michigan and Conference Board surveys continued to rise sharply in April. In a high-volatility inflation environment, expectations tend to respond more to inflationary than disinflationary shocks. Wall Street often dismisses consumer surveys, but firms, households, and traders all have skin in the game—unlike some forecasters. Academic research, including my own, shows these expectations help forecast inflation. No measure of inflation expectations is perfect and thus aggregation beats cherry-picking.

In April, besides further increases in one-year inflation expectations from these consumer surveys the Atlanta Fed BIE also indicated notably higher year-ahead inflation expectations amongst firms in April. The chart above captures the common trend across firm and household expectations, incorporating April and March data. It suggests "Main Street" inflation expectations rose from 2.4% y/y PCE in Q4 to 3.3% in March. April data imply a jump to 4.2%—similar to the acceleration we saw in Q2–Q3 2021. This reinforces that firms and households remain uneasy about near-term inflation amidst persistent policy uncertainty.

The University of Michigan survey also measures 5–10 year inflation expectations amongst consumers, and this held at 4.4% in April (unrevised from prelim), up from 4.1% in March. The chart above shows that long-run expectations have been structurally higher post-COVID than in 2016–2019, with more respondents expecting above-average inflation. A similar, though milder, tilt existed in 2002–2007, pre-Great Recession. Since 2021, this longer-term bias has mirrored the early 2000s. In H2 2024 and early 2025, elevated monetary, fiscal, immigration, and trade policy uncertainty pushed it to a new high in February—going back to 1979. It eased a bit in March but remains historically elevated.

To gauge how restrictive the Fed’s interest rate policy is perceived to be for the year ahead, I published back in August 2023 an analysis that focused on a one-year survey-based real interest rate. This rate is calculated by taking the monthly average of daily one-year interest rates and subtracting the (monthly) common inflation expectations factor from the inflation expectations chart discussed in the previous section that is scaled in year-on-year PCE inflation terms.

Key to assessing the restrictiveness of these one-year real rates is where neutral real rates are heading. The chart above is an update of an earlier chart and shows that after close to a decade of ultra-low neutral real rates, these rates have trended up since 2016. Throughout most of 2024 and up to now in 2025, these R* estimates plateaued with the average and median across the proxies sitting at around 1.5% and 1.3% respectively in April, above the median 1% rate from the Fed’s March SEP.

The chart above compares the one-year survey-based real interest rate with the R* range across the various market- and model measures as a perceived policy stance measure. While back in February this measure already pointed to an expectation that the Fed’s policy stance would become accommodative in inflation-adjusted terms over the year, this became even more dramatically the case by April.

Some of this easing in perceived monetary policy stance came about through a declining one-year nominal rate between February and April of around 25bps. But most of the expected stance easing is due to the firming in near-term “Main Street” inflation expectations mentioned earlier, as these increased between February and April by about 150bps. Most Fed officials have expressed in public remarks their desire to keep rates on hold while assessing recent inflation trends and the uncertainty regarding new policy initiatives out of D.C.:

“[…] given that the demand for investment capital will likely be lower and push short-run r* down, policy is getting somewhat tighter on its own, reducing the immediate need to raise the federal funds rate to keep long-run inflation expectations anchored.“ N. Kaskari, Potential Implications of Announced Tariffs for Monetary Policy, April 9, 2025.

But with a lot of easing in the perceived monetary policy stance due to a pickup in inflation expectations this will not be welcomed by Fed officials. The possible easing impact of these developments could make their job of anchoring inflation expectations harder, so at the very least FOMC officials, IMO, will want to guide rates to remain elevated by signaling persistently unchanged policy rates to counter this potential effect.

So, overall developments in the economy right up to the eve of “Liberation Day” remain solid. However, survey-based inflation expectations have exhibited a broad-based and notably firming. Even if some surveys overstate the role of uncertainty, the broad-based rise in expectations signals heightened concern about inflation volatility. Disinflation is being discounted. Combined with underlying trends in the “hard” inflation data still pointing to a persistently above-2% pace of price increases, "looking through" inflationary tariff effects thus is becoming harder for the Fed— and depends on how much labor market weakness they’re prepared to tolerate.

Meeting Postmortem

As expected, the FOMC decided for the third consecutive meeting to keep the Fed funds rate target range unchanged at 4.25%-4.50%. The post-meeting statement singled out even more than in the previous statement the uncertainty in the economic environment due to the current administration’s tariffs policy:

Recent indicators suggest that economic activity has continued to expand at a solid pace.Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run.

Uncertainty around the economic outlook has increased.Uncertainty about the economic outlook has increased further.

The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities.

Beginning in April, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion.

The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Adriana D. Kugler; Alberto G. Musalem;

and Jeffrey R. Schmid.and Christopher J. Waller. Neel Kashkari voted as an alternate member at this meeting.Voting against this action was Christopher J. Waller, who supported no change for the federal funds target range but preferred to continue the current pace of decline in securities holdings.FOMC Statement, May 7, 2025 (with annotations relative to the March FOMC Statement).

Chair Powell’s remarks highlighted the stagflation risks stemming from, in particular, the current administration’s trade policy. The Fed is highly uncertain about which side of its mandate faces the highest adverse risk. However, as Chair Powell frequently pointed out, the current economy is, from the Fed’s perspective, still performing solidly and in a fairly good shape. This, in turn, allows the Fed to be patient and wait for incoming data to better assess which of the elevated risks (i.e., risks of higher inflation vs that of higher unemployment) is becoming more worrisome.

According to Chair Powell the aforementioned assessment will focus on: (i) how far either inflation or the unemployment rate are overshooting their long-run rates, and (ii) how long it would take for inflation or the unemployment rate to return back to their respective desired levels conditional on no further Fed policy rate moves. The Chair remained confident that incoming data could provide a timely indication which way these risks will evolve.

As has been traditional over the past year, Powell continued to reiterate that in dealing with these risks future policy rate decisions still will be between keeping rates constant or cutting them, as he still sees the Fed’s policy stance as notably restrictive although my discussion in the previous section sheds some doubt on that view. However, given the large-scale tariff hikes it is more likely than not that the “hard data” will fairly soon indicate that the above “worrisome” condition (i) will hit inflation while not necessarily (yet) for the unemployment rate. And given already elevated inflation expectations it also would be unlikely that such a highly elevated inflation rate will take a while to come back to target, thus violating the aforementioned “worrisome” condition (ii). Given the Chair’s comments this likely indicates no change in the Fed funds rate this year.

The chart above also suggests that a differentiation between the 2025 core inflation path implied by the March SEP and those based on a variety of assumed average month/month rates would likely become more apparent in the May and June data. Based on that chart the modal outlook for the June FOMC meeting is that of an unchanged Fed funds rate. I can only see the Fed deciding to cut rates in June if May year/year core PCE inflation slows below 2.6% as this would imply a potential 2025 core PCE inflation that undershoots the March SEP forecast.

To summarize:

Going into this meeting we have a still solid real economy, especially after discounting the distortion of elevated tariff fears-induced imports, still elevated underlying inflation trends and rapidly rising “Main Street” inflation expectations.

The Fed expects stagflation to be a feature of the U.S. economy in 2025 but is unsure which of its inflation or employment mandates will be more adversely affected.

Given that the large-scale tariff hikes will likely more quickly impact inflation than the labor market, and that the already elevated inflation expectations could make this inflation impact more persistent, it’s very unlikely that the Fed will change policy rates or maybe not until year-end.

My modal outlook for 2025 is therefore now for no rate cuts, down from one rate cut previously, with a tail risk of a single rate cut by the end of the year (November or December FOMC meeting).